Information Gaps

Information Gaps

For a market to work efficiently, producers and consumers need accurate and complete (sometimes called ‘perfect’) information about the prices being charged by other firms and the quality of the goods on sale. This is often not the case. When you go shopping, how confident are you that you have bought the items at the lowest price available? Sometimes it is very difficult to discover the best price available, although online shopping makes this much easier.

The internet does help to address information problems, through price comparison websites and people posting reviews, but this is not a complete solution to the problem. Not all reviews are genuine or impartial (they may be negative reviews posted by competitors, for instance).

A more intractable information problem is to do with quality of goods rather than price. Consumers are often at a disadvantage compared to producers. Economists call this the problem of asymmetric information, where one party to the transaction (usually, but not always the seller) has much better knowledge of the product than the other party. Persuasive and misleading advertising can add to this problem.

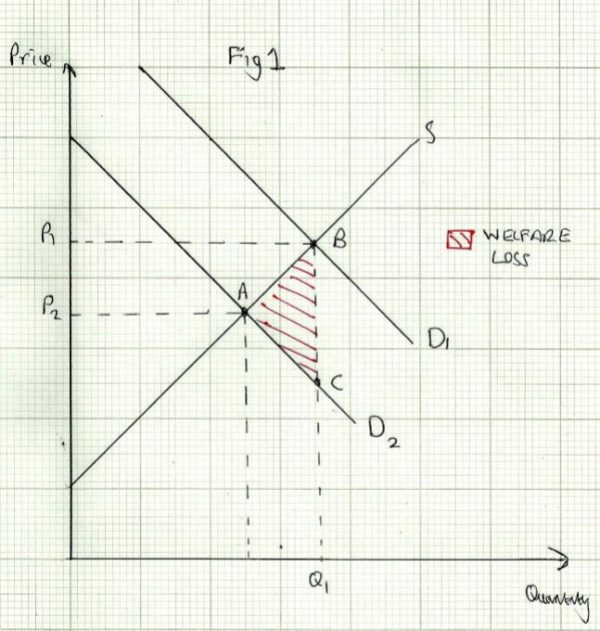

As a result of imperfect information problems, some goods (expensive and shoddy) may be produced instead of cheaper, better alternatives. The former are being over-produced and the latter under-produced. In effect, the demand curve can shift outwards as a result of imperfect information, as consumers over estimate the benefits they will derive from purchasing the good or service. The price and market quantity will therefore be higher than would be the case if consumers had more complete information. This is shown in _Fig 1 _below:

__D1 __shows the demand curve with imperfect information, leading consumers to over estimate the benefits of consuming the good. __D2 __shows the demand curve that would apply if consumers had accurate information. Triangle __ABC __shows the welfare loss as a result of the over consumption.

Examples

Healthcare: In private medicine for instance, it may be very easy for doctors to prescribe expensive treatment which is either not needed at all, or no more effective than cheaper alternatives. This can increase the income and profits for the hospital at the expense of the patient.

The problem is less likely to occur in a publicly financed healthcare system such as the NHS, because doctors and hospitals have a limited budget to spend on treating their patients, and do not benefit financially by providing unnecessary or expensive treatment.

Education: In the UK universities behave increasingly like commercial organisations. They rely on student fees for their income, and so have to try to attract students to take their courses. Not all university courses are of equal quality, or give students a good chance of high earnings in their careers. Yet nearly all universities charge the maximum £9000 a year in fees that are currently allowed. Students may be attracted by high pressure marketing rather than genuine and accurate information about the quality of the courses on offer.

The problem is addressed to some extent by forcing universities to publish statistics on things like the % of students who drop out, employment after graduation, staff/student ratios and so on.

Financial services: such as mortgages, life insurance and pensions are very complicated for many people to understand, and they may take it on trust that banks and other financial institutions are acting with integrity when they sell these products.

There have however, been a number of scandals over mis-selling of financial services in recent years, with banks being forced to pay customers compensation for mis-selling, particularly over so called ‘payment protection insurance’ (PPI), where customers taking out loans were also persuaded to take out an insurance policy to pay back the loan if they fell into hardship. These policies often turned out to have a lot of ‘small print’ clauses which made it very difficult for people to claim on them when they needed to.

Because of the complex nature of financial services, many people use a financial advisor or broker to help them choose an appropriate product. This can lead to the so called __principal-agent __problem.

The __principal __is the individual or organisation that may benefit or lose from a transaction. The __agent __is the person or organisation acting for them. In this case the person using a financial advisor is the principal, and the advisor is the agent. The problem here is that the agent and principal do not necessarily have the same interests. The advisor may seek to persuade the client to take out a particular mortgage policy because he (the advisor) will earn a large commission from the bank selling it. Again this is a case of asymmetric information (the advisor knows more than the client) and it can lead to market failure and misallocation of resources.