Price Determination

The Market or Equilibrium Price

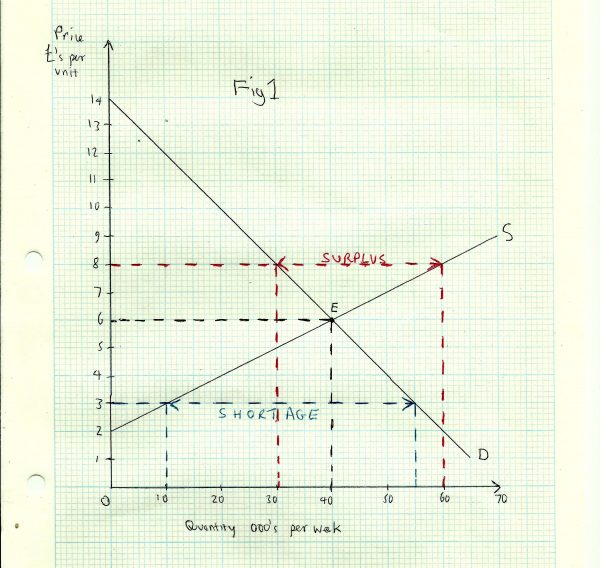

The price of a good is determined by the interaction of demand and supply in the market. This can be shown by putting the demand and supply curves on the same diagram. See _Fig 1 _below:

There is just one price (£6.00 per unit), where the quantity demanded and the quantity supplied are equal (at 40,000 units per week). This is called the market or equilibrium price. It is the price at which the market will settle, provided that there are no changes in the conditions of demand or supply.

At the market price, consumers want to buy everything that producers want to sell. There is neither a shortage (unsatisfied demand), or a surplus (unsold goods).

We can show how a market moves towards equilibrium by considering what happens if the price is above or below the equilibrium.

Let us suppose that price is currently £8.00 per unit. At this price quantity supplied (60,000), exceeds quantity demanded (30,000). There is a surplus of unsold goods of 30,000 units per week. In order to sell these unsold goods, some producers will start to reduce price. This will cause demand to expand, but supply will contract, as some producers (the least efficient ones) will exit from the market as they can’t make a suitable profit.

Price will continue to fall until the surplus has been eliminated. This happens once the price has fallen back to £8.00.

If the price is currently £3.00 per unit, we can see from Fig 1 that quantity demanded (55,000), exceeds quantity supplied (10,000 units) This time there is a shortage in the market of 45,000 units per week. Buyers will be competing with each other for scarce goods, and suppliers will see that they have the opportunity to raise price. As price rises, demand will contract, but supply will expand, as the good is more profitable for producers. Price will continue to rise until it reaches £8.00, where there is no longer a shortage.

Changes in the Conditions of Demand or Supply

_Fig 1 _shows a market in static equilibrium; the conditions of demand and supply are stable, so the market will settle at a price of £8.00. But most markets are not static. The conditions of demand and supply are constantly changing. This means that price is also likely to be changing, as the market seeks to adjust to new conditions. Good examples of such markets include stock markets and foreign exchange markets. The prices of shares and currencies change almost minute by minute.

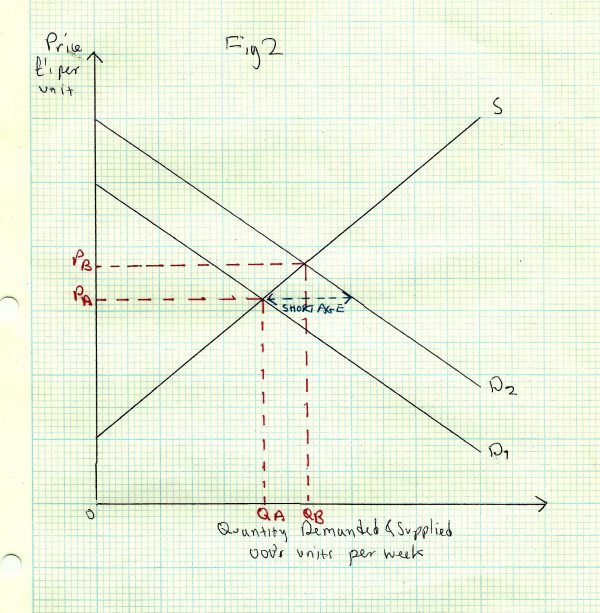

_Fig 2 _shows the effect on market price and quantity when the conditions of demand change.

The market is initially in equilibrium at price PA __and quantity __QA. A shift outwards of the demand curve from D1 __to __D2 represents an increase in demand at all prices. There will therefore be a shortage, causing price to start to rise. Demand will contract along D2 __and supply will expand. The new equilibrium will be at price __PB __and quantity __QB.

A decrease in demand, from D2 __to __D1 would result in a fall in price from PB __to __PA __andfall in quantity from __QB __to __QA.

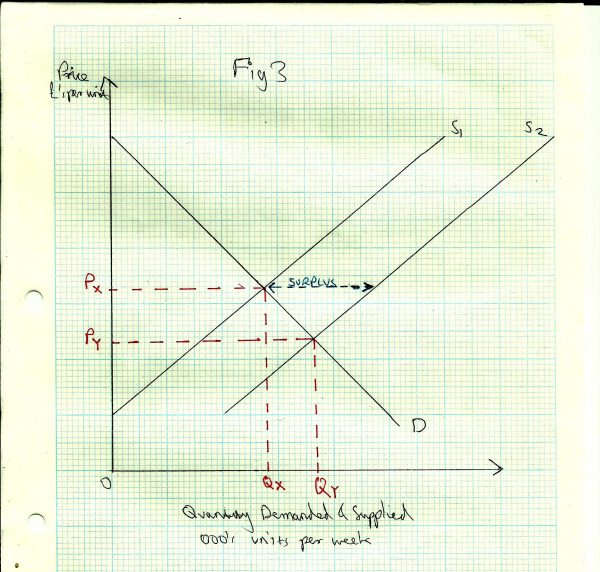

_Fig 3 _shows the effect on market price and quantity when the conditions of supply change:

The market is initially in equilibrium at a price of PX __and quantity __QX. A shift outwards of the supply curve from S1 __to __S2 __represents an increase in supply at all prices. There will therefore be a surplus, causing price to start to fall. Supply will contract along __S2 __and demand will contract. The new equilibrium will be at price __PY __and quantity __QY.

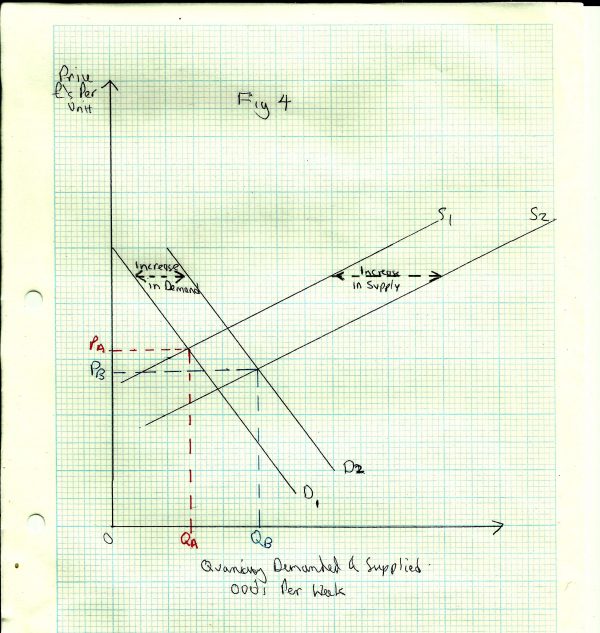

_Fig 4 _shows the effect on market price and quantity when the conditions of both demand and supply change:

An increase in both supply and demand is shown by the movement of demand from D1 __to __D2, and a movement of supply from S1 __to __S2. This will result in an increase in market quantity from QA __to __QB.

The effect on price depends on the relative increases in supply and demand. In Fig 4, supply has increased more than demand, so price has fallen from PA to PB.If demand had increased more than supply, then price as well as quantity would have risen. If demand and supply had increased by the same amount, price would be unchanged and only quantity would increase.

If demand and supply both decreased (moving back to the left, then quantity will definitely decrease, but again, the effect on price depends on the relative decreases in demand and supply. In _Fig 1 _a decrease in demand from D2 __to __D1 together with a decrease in supply from S2 to S1 __results in a rise in price (from __PB __to __PA) because supply has decreased more than demand.

Why Markets do not Always Clear

As we have seen the equilibrium price is the price at which there is no shortage or surplus. This is sometimes also called the market clearing price. Neo-classical economists argue that this will happen provided the market is truly ‘free’; i.e. not subject to government intervention or anti-competitive behaviour by producers or consumers. In many cases this condition is not met. A national minimum wage, for instance, may keep the price of labour (wages) permanently above the equilibrium level, resulting in a ‘surplus’ of unemployed workers who are willing, but unable to find employment.

Producers can also sometimes collude to keep the price above the market clearing price, by forming a cartel.