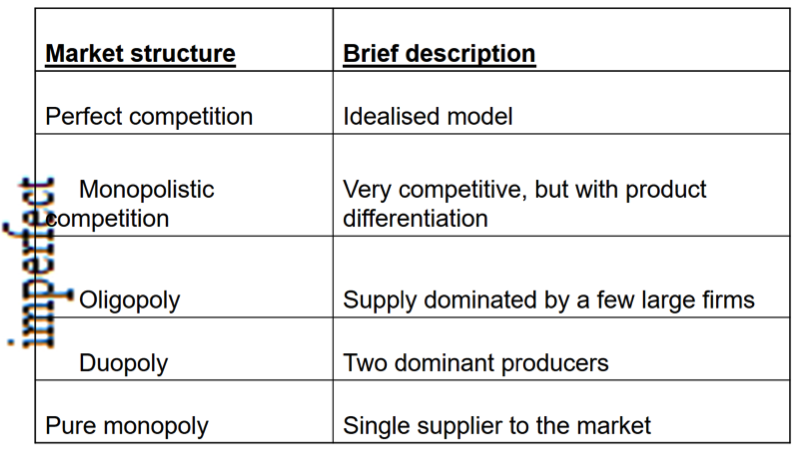

Spectrum of Competiton

Spectrum of Competiton

Please note what the Getting Started Guide has to say about the Theory of the Firm/Market Structures diagrams!

Imperfect competition are monopolies, oligopolies, duopoly and monopolistic competition.

Perfect competition and a pure monopoly are at either end of a spectrum of market structures. There are relatively few if any industries which conform to the strict characteristics of these two models. Most industries fall somewhere in between because:

-

Competition exists because there’s at least two firms in the industry.

-

Competition is imperfect because firms sell products which are not identical to the products of rival firms (i.e. product differentiation occurs).

The economic theory of perfect competition was born in the latter half of the 19th century when, arguably, this market structure was ripe and homogenous products were the norm. In the 20th and 21st century fewer and fewer industries can be said to be perfectly competitive, so a number of theories of imperfect competition have been advanced to explain the behaviour of firms – resulting in our ‘spectrum of competition’.

Monopoly

A pure monopoly is a single supplier in a market. For the purposes of regulation, monopoly power exists when a single firm controls 25% or more of a particular market.

Formation of Monopolies

Monopolies can form for a variety of reasons, including the following:

-

If a firm has exclusive ownership of a scarce resource, such as Microsoft owning the Windows operating system brand, it has monopoly power over this resource and is the only firm that can exploit it.

-

Governments may grant a firm monopoly status, such as with the Post Office, which was given monopoly status by Oliver Cromwell in 1654. The Royal Mail Group finally lost its monopoly status in 2006, when the market was opened up to competition.

-

Producers may have patents over designs, or copyright over ideas, characters, images, sounds or names, giving them exclusive rights to sell a good or service, such as a song writer having a monopoly over their own material.

-

A monopoly could be created following the merger of two or more firms. Given that this will reduce competition, such mergers are subject to close regulation and may be prevented if the two firms gain a combined market share of 25% or more.

Key Characteristics

-

Monopolies can maintain super-normal profits in the long run. As with all firms, profits are maximised when MC = MR. In general, the level of profit depends upon the degree of competition in the market, which for a pure monopoly is zero. At profit maximisation, MC = MR, and output is Q and price P. Given that price (AR) is above ATC at Q, supernormal profits are possible (area PABC).

-

With no close substitutes, the monopolist can derive super-normal profits, area PABC.

-

A monopolist with no substitutes would be able to derive the greatest monopoly power.

Perfect competition

Perfect competition can be used as a yardstick to compare with other market structures because it displays high levels of __economic efficiency and is the closest thing we have to a level-playing field. __

Some commodity markets such as tea and sugar are pretty close to being perfectly competitive – other commodity markets such as diamonds/oil are not thanks to cartels and government intervention/failure.

We assume that a perfectly competitive market produces homogeneous products – in other words, there is little scope for innovation designed purely to make products differentiated from each other and allow a supplier to develop and then exploit a competitive advantage in the market to establish some monopoly power.

A contestable market provides the discipline on firms to keep their costs under control, to seek to minimise wastage of scarce resources and to refrain from exploiting the consumer by setting high prices and enjoying high profit margins. In this sense, competition can stimulate improvements in both static and dynamic efficiency over time.

The long run of perfect competition, therefore, exhibits optimal levels of economic efficiency. But for this to be achieved all of the conditions of perfect competition must hold – including in related markets.

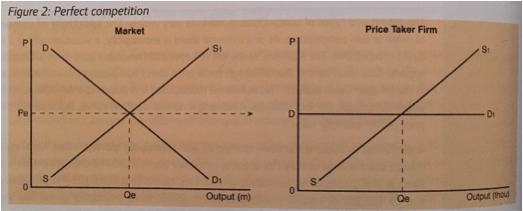

The equilibrium point where demand meets supply will be the point at which the cost of an extra unit just matches the utility (satisfaction) it offers, which means that the ideal quantity of scarce resources are used for the product. The situation is summarised in the diagram below:

Should demand for the product increase, the demand curve would shift to the right and the ‘price signalling mechanism’ would occur. High prices show profits to be made and thus supply would increase to the market as well (existing firms increase output and new firms are attracted). As a result, supply shifts to the right too which is the market mechanism at its best with things returned to an equilibrium once more offsetting the initial price rise and returning things to a ‘normal profit’.

Evaluation of monopolies

The Advantages of Monopolies

Monopolies can be defended on the following grounds:

-

They can benefit from economies of scale, and may be ‘natural’ monopolies, so it may be argued that it is best for them to remain monopolies to avoid the wasteful duplication of infrastructure that would happen if new firms were encouraged to build their own infrastructure.

-

Domestic monopolies can become dominant in their own territory and then penetrate overseas markets, earning a country valuable export revenues. This is certainly the case with Microsoft.

-

According to Austrian economist Joseph Schumpeter, inefficient firms, including monopolies, would eventually be replaced by more efficient and effective firms through a process called creative destruction.

-

It has been consistently argued by some economists that monopoly power is required to generate dynamic efficiency, that is, technological progressiveness. This is because:

-

High profit levels boost investment in R&D.

-

Innovation is more likely with large enterprises and this innovation can lead to lower costs than in competitive markets.

-

A firm needs a dominant position to bear the risks associated with innovation.

-

Firms need to be able to protect their intellectual property by establishing barriers to entry; otherwise, there will be a free rider

-

Why spend large sums on R&D if ideas or designs are instantly copied by rivals who have not allocated funds to R&D?

-

However, monopolies are protected from competition by barriers to entry and this will generate high levels of supernormal profits.

-

If some of these profits are invested in new technology, costs are reduced via process innovation. This makes the monopolist’s supply curve to the right of the industry supply curve. The result is lower price and higher output in the long run.

The Disadvantages of Monopoly to the Consumer

Monopolies can be criticised because of their potential negative effects on the consumer, including:

-

Restricting output onto the market.

-

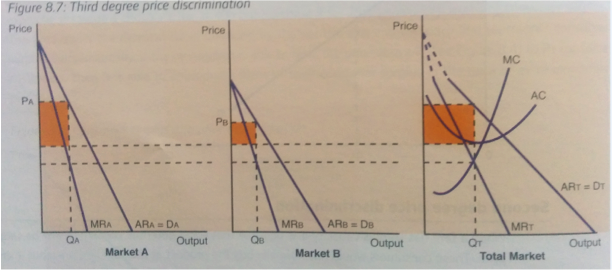

Charging a higher price than in a more competitive market (price discrimination also, see overleaf)

-

Reducing consumer surplus and economic welfare.

-

Restricting choice for consumers.

-

Reducing consumer sovereignty.

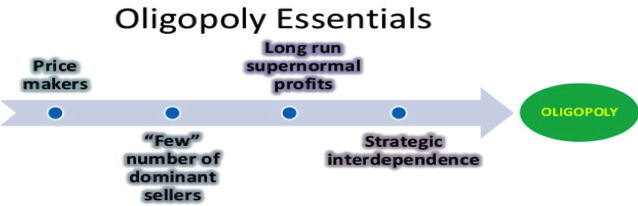

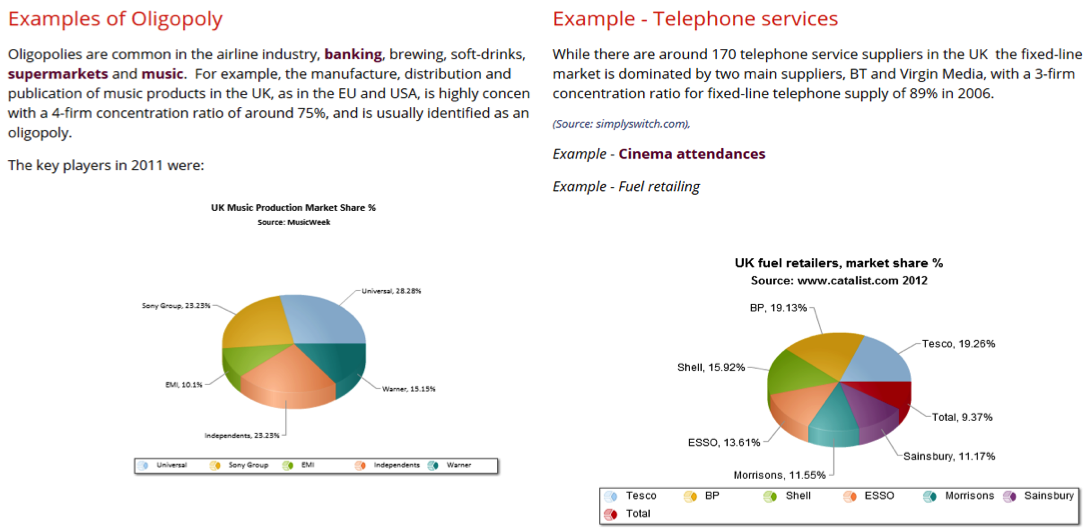

Oligopolies and their importance

Most markets are said to be imperfectly competitive. A few are monopolistically competitive (e.g. hairdressers, plumbers etc.,) but the majority are concentrated markets, dominated by a few suppliers – i.e. an oligopoly. Therefore the theory on the market structure of an oligopoly is arguably the most important of the theories of the firm.

Oliopoly market structure

For an industry to be classified as an oligopoly there must be two key aspects of its market structure:

-

Supply in the industry must be concentrated in the hands of a relatively few number of firms. Generally speaking we draw the combined concentration ratio of the 3/4/5/6/7 firms dominating the market at more than 60% market share in order to be classified as an oligoploly.

-

Firms must be interdependent. The actions of one firm will directly affect another. In perfect competition firms are independent – if one farmer decides to grow more wheat this does not affect his nearest competitor nor market prices. In an interdependent oligopoly however, if one large firm decides to pursue policies to increase sales, this is likely to be at the expense of other firms in the industry.

-

There are barriers to entry to the industry. If there weren’t, firms would enter the industry to take advantage of the abnormal profits and would reduce the market share of the dominators.

The theory of monopolistic competition makes almost the same assumptions as that of perfect competition – the key difference being that products are differentiated and thus branding is important!

Differences in products create scope for brand loyalty, therefore a consumer might be willing to pay a higher price for the product of one firm compared to another in the market (e.g. Tony and Guy vs Marden’s barber!). Therefore, monopolistically competitive firms are not price-takers (unlike perfect competition where they are and have a horizontal demand curve as a result). Thus each firm is faced with a downward sloping demand (AR) curve. Also, because of the highly competitive nature of the market and the vast array of substitutes available, the demand curve will be much more elastic (i.e. shallow) than it would be for a monopoly (inelastic = steep) market structure.

Relatively few industries possess the above 4 characteristics. Most industries have concentration ratios which would suggest they were oligopolistic in character. However, examples might be local hotels, coach travel, furniture making and, the classic, hairdressers. It is often confusing to students that a market structure with so little monopoly power for the firms is called monopolistic competition. The term ‘monopolist’ refers to the small degree of monopoly power each firm possesses as a result of selling a branded product – e.g. Tony and Guy.

Relatively few industries possess the above 4 characteristics. Most industries have concentration ratios which would suggest they were oligopolistic in character. However, examples might be local hotels, coach travel, furniture making and - the classic - hairdressers. It is often confusing to students that a market structure with so little monopoly power for the firms is called monopolistic competition. The term ‘monopolist’ refers to the small degree of monopoly power each firm possesses as a result of selling a branded product – again, Tony and Guy!