How Small Firms Compete

The role of small businesses

Although large businesses employ many people, most businesses are small. Large companies are only in their thousands, whilst small businesses are in their millions. Around half of UK output is produced by small and medium-sized enterprises (SMEs, which employ <250 employees). As we have discussed there are many reasons why small businesses exist and thrive. For many products, it is possible for large companies to flourish side-by-side with much smaller ones, as is the case with coffee shops.

Start-ups

Start-up businesses are generally small because they have access to limited funding. An entrepreneur’s own resources will normally be insufficient to fund a large-scale business. Furthermore banks will see starting from scratch on a large-scale as extremely risky. A number of businesses will grow into larger ones (e.g. Bannatyne’s care homes), some will fail and some will be quite successful whilst staying small.

Small-firm survival in competitive markets

Product differentiation and Unique Selling Points

Some small businesses produce homogeneous products (i.e. identical). Most businesses differentiate their products, they do not compete only on price. A ‘better product’ can command a higher price. There can be varied prices for even slightly differentiated products. Small firms can compete if their differentiated products have non-price advantages. E.g. the market for potatoes (homogenous) versus the market for cars or mobile phones (differentiated).

So it is important to differentiate yourself from the competition and attain a USP. A good example is the bread market where 3 firms dominate (an oligopoly – Warburtons, Hovis and Kingsmill). In the past year they had lost 121 million worth of sales due to competitors successfully attaining product differentiation and USP, thus stealing market share. People seem to be eating different types of bread, but also as incomes grow again people are choosing to eat more alternatives to bread.

Artisan bread is different (the jury is out on whether it is tastier, better for you or longer lasting). Being different will appeal to some consumers – thus attaining product differentiation is important. The fact that ‘artisan bread’ is more expensive is not necessarily a disadvantage as it can sometimes provide a USP. Being handmade is also a useful USP (e.g. jewellery). There are many ways for small firms to differentiate successfully, creating their own markets. Thus product differentiation/developing a USP can enable a small firm to successfully compete.

Flexibility

Large businesses are vulnerable to diseconomies of scale (2.1.1 recap!) due to communication/co-ordination/morale problems. Smaller firms are more flexible – they can respond more quickly/accurately to their customer’s preferences. Products/services can be modified to meet unique customer needs. Flexibility can provide a very important way for small firms to compete.

Customer service

Where demand is limited there is little point in expansion, even if economy of scale (m, t, f, p and mktg) could be available. Small corner shops will always exist and survive for those customers who are too poor to commute to the big players, or perhaps its too inconvenient as well. They also offer convenient ‘top up shopping’ for odd items forgotten on your major shop! Though in the modern day it is believed that the small store has some hidden advantages over the big store. In the developed world, large stores can offer up to 60,000 different items.

Research shows that in MEDCs the average consumer has 22 minutes to shop and we simply can’t see such a vast range of products in that time. Thus the advent of the ‘express store’. After years of steady growth in retail store size, in 2007 the average size of a US grocery store dipped slightly. We seem to prefer smaller stores with a more personal customer service. Another good example is personal trainers versus mass produced ‘fitness DVDs. A personalised customer service can enable small firms to compete successfully.

Relationships

Some entrepreneurs will choose to stay small, even where there is promising growth potential! It all depends on their entrepreneurial motives and business objectives (1.2.2). Some entrepreneurs want to stay at a level where they can closely control all aspects such as dealing with customers, suppliers and employees. They might see large business as too stressful and don’t value extra profits over control/independence. Some might even be social entrepreneurs!

Many of the points identified here depend of the relationship between client and supplier – a relationship of trust can ‘add value’. From a consumers (and even a business’s!) point of view, the loss of the personalised relationship can outweigh the savings from switching to a larger, cheaper supplier. Many of the largest firms are commonly ranked low in customer satisfaction surveys – thus a closer relationship with their stakeholders can be another way that small firms can compete successfully.

__Niche market __

Lastly in relation to demand, there are highly specialised niches catering for minority interests, where the total demand nationally and maybe even globally might be insufficient to allow firms to exploit E of S. For example hobbies such as falconry. There is simply not the demand available to occupy large businesses. Thus small firms can compete in a niche market, where the segment is so small/unique that they remain a small firm.

Small firm objectives

In closing, some small firms choose to remain small for a reason. In Theme 1 (1.1.2) we looked at business objectives – profit is not the objective for all! Some are happy to be profit satisficing, others to be ethical/social objectives. This is perhaps easier to achieve in a small firm – as the bigger you get the harder these become to maintain, along with divorce of ownership and control.

Exam style question: Lessons in Economics from the UK Grocery Market

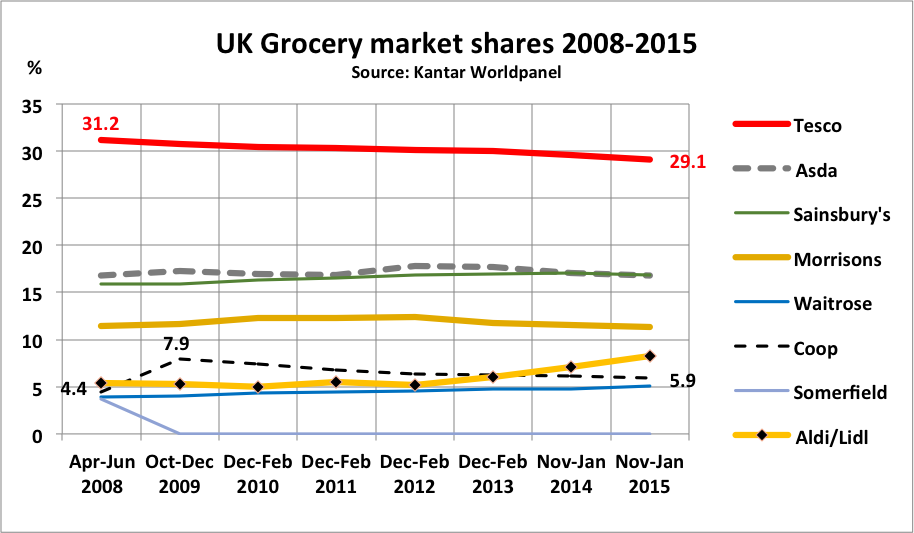

The very latest figures for the UK grocery sector show the continuation of several trends, from the rise of the discounters and also Waitrose, through to the decline of Tesco and the Coop.

Part of the reason Tesco’s problems have had such publicity is because it’s the market leader – and there’s a natural inclination to assume that dominant companies can cash in on the strength of their position.

As shown in the graph, none of the Top 4 have found things easy, especially since early 2012, when the Aldi-Lidl bandwagon began. It is at least as interesting to note though that the Coop’s decline since 2009 easily outweighs the decline of any other retailer.

In July 2008 the Coop (the UK’s 5th largest grocery business) bought Somerfield, the country’s__ 7__th__ largest chain. Coop paid £1.57 billion for Somerfield’s 900 stores and its __3.7% share of the grocery market. As the Coop had a 4.4% share at the time, it could hope to end up with around an 8% share – quite close to the 11% share of Morrisons supermarkets, the 4th__ of the Big Four__.

At the time the Coop chief executive Peter Marks said that the acquisition of Somerfield would provide ‘rocket fuel’ for his group’s growth plans. He went on to say that the deal would “create a stronger fifth player in food and a convenience store chain with unrivalled geographic reach”. The Coop also said that it aimed to double its profits over the next 3 years. Its 2007 profit had been £195.5 million, sharply down on 2006’s £360 million.

Peter Marks wasn’t the only person with good things to say about this takeover. Retail experts ‘Verdict Research’ said that “The benefits of this move are that they have a larger scale, and it propels them int_o a different league in terms of food retailing”._

By December 2009 Peter Marks was trumpeting the success of the takeover, proclaiming that “We’ve gone from the second division back into the Premiership. Overnight we doubled our share of the UK supermarket sector.” In mid 2010, however, the Coop half-yearly report cited ‘inevitable disruption’ in the integration process as the explanation for a fall in sales at former Somerfield outlets (now converted to the Coop brand).

A year later and Peter Marks admitted to a 3.4% fall in like-for-like sales across the Coop grocery business, partly due to ‘disruption to store activity’. Nevertheless he claimed to be very confident that the bigger scale of the business would allow successful investment, such as in new software that would provide improved stock management. Despite this optimism, in the summer 2012 he retired as Chief Executive – leaving before the massive financial problems at the business became clear later in the year.

As for the Coop’s attempt to join the big 5 grocers: from a high of 7.9% market share just after the merger, by early 2015 the figure was down to 5.9%. The £1.57bn paid for Somerfield was a waste of money. And how did it all work out for Peter Marks?

Well, from £609,000 in 2007, his remuneration jumped to £1.4m in 2008, £1.56m in 2009 and £2.12m in 2010. Nice work, if you can get it. But as shown in the table below, for the Coop the results were little short of disastrous.

Questions (30 marks; 35 minutes)

__Question 2: __Explain how the Coop’s purchase of Somerfield can be termed ‘horizontal integration’. (4 marks)

__Hint: __4 Marks = 4 things. Define, State, Link and Explain.

Key concepts at the end of the lesson.

__Question 3: __Explain what the Coop might have expected from a horizontal takeover. (4 marks)

Key concepts at the end of the lesson.

__Question 4: __Discuss the motives of Peter Marks in choosing the takeover of Somerfield as the best way to achieve growth. (8 marks)

Key concepts at the end of the lesson.

__Question 5: __Between 2009 and 2015 Waitrose built its market share from 4% to 5.1%, without using takeovers. The Coop spent £1.7bn but without financial success. Assess growth strategies in the grocery sector. I.e., evaluate the approach of organic growth and inorganic growth in this sector - which do you recommend? (12 marks)

Key Concepts

Question 2 Key Concepts

- Horizontal integration is when a business acquires another in the same industry and at the same stage of production, in other words a direct competitor. That is exactly Coop and Somerfield’s position in the grocery market.

Question 3 Key Concepts

-

It could expect economies of scale, that is lower average costs as a result of having higher sales and therefore higher purchasing/production; in grocery retailing purchasing economies (bulk buying) would be the most obvious, though there might also be technical economies from being able to afford state-of-the-art software as Tesco was always supposed to have had via its Clubcard.

-

It would have two pools of management to draw from when deciding on the future of the business, e.g. two marketing directors, only one of whom would be needed in future; the evidence from the market share and profit data suggests that this was nothing like as valuable as might have been expected.

Question 4 Key Concepts

-

Peter Marks sought to make the Coop a strong 5th in the grocery market, using the Somerfield takeover to propel Coop towards 8% market share (quite close to Morrisons); without a takeover bid the growth would have had to come organically, taking a long time (lots of new stores means lots of planning permissions and lots of cash); the success of Waitrose in recent years shows that this approach is perfectly sensible.

-

Although there are rational reasons for the takeover, outsiders cannot know whether ego/self-promotion or pure self-interest played a part. Did Peter Marks want to ‘make his mark’ by buying Somerfield? Or did he want to achieve a level of growth that would justify big financial rewards for the Coop’s chief executive? The evidence shows that he did very well personally out of the Coop’s expansion.

-

Marks wouldn’t be the first chief exec to assume that a jump in scale automatically yields economic benefits from bulk buying and a stronger bargaining power; but it seems at least as likely that he was pursuing a personal rather than business agenda.

Question 5 Key Concepts

-

Growth is a standard business objective; many think it’s a form of deferred profit-seeking, i.e. today we grow, tomorrow we dominate and the day after we get our financial payoff.

-

Why firms grow could be for the above reason or could be more personal; bosses like to ‘make their mark’, that is to demonstrate that their period of office yielded long-term benefits for the business; growing Waitrose to become a ‘national treasure’ among retailers probably yields personal satisfaction for the boss concerned.

-

There is also the view that if you’re standing still, you’re falling back and therefore making yourself vulnerable, perhaps to a take-over bid; so avoiding being bought up by others becomes a justification for growth.

-

If why is one puzzle, how is another. Waitrose, Aldi and Lidl have been growing in two ways (though both are regarded as ‘organic’). They have been enjoying higher sales per store (rising ‘like-for-likes’) and also opening lots of new stores. Opening new stores is fine if they’re profitable, which they probably are for Aldi and Lidl. Waitrose is more of a mystery, because the more it grows the_ less_ profitable it gets – so probably it’s opening too many Convenience and motorway stores

-

The alternative to organic is inorganic growth, for example takeovers; the Coop has left a classic case study in what not to do. Buying up a weak rival gave twice the problems rather than twice the benefits. This is not unusual as research still shows that the majority of takeovers lead to long-term negative economic benefits.

- Question 1: Define inorganic growth

- Your answer should include: Mergers / Takeover / Joint Ventures