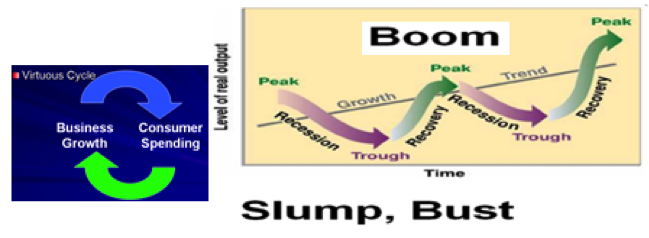

The Economic Cycle

What is an Economy?

The production and consumption of goods and services in a country. Check this Wikipedia page for more details about the UK Economy.

What is Economic Growth?

When a country’s Gross Domestic Product (GDP – total value of output of goods and services in a country in a year) increases.

If government manages to juggle of the 5 juggling balls (1.2.5!) successfully, they achieve Economic Growth.

An economy grows when the total level of output of goods/services in a country increases (i.e. its GDP).

When a country’s GDP is falling, it has no economic growth. This is a Recession. This causes problems:

-

As a country’s output is falling, fewer workers are needed. What will happen?

-

Will there be pay rises? Real income will decrease as business is not good and businesses cannot give their employees pay rises. The average standard of living (number of goods/services people can afford to buy in one year) will decline.

-

Businesses will not expand their firms due to lack of money. More importantly, there will not be the demand from their customers to expand.

Characteristics of a Boom

A boom is when real national output (GDP) is rising strongly at a fast rate. In boom conditions, real output and employment increase as well as aggregate demand (AD = total demand in an economy) for goods/services.

Economic Cycle

When we talk about a trend, we ignore fluctuations which are an important feature of economic development over time. Economies rarely grow (or even decline) at a consistent rate. E.g. 2000-2007 in the UK was relatively steady growth. In 2008 output fell so fast that it took 6 years to recover to 2007 levels! Economies are cyclical so recession is inevitable, but the GFC made the past recession a lot worse!

Boom

Faster growth can ‘snowball’ into a boom. Firms seek to rapidly increase output as demand is increasing, so employment will be high. Competition for skilled workers will mean pay increases. U/E will be low and consumer confidence will boost spending. A feature of the UK/USA economies is that in the book times people borrow more ‘to keep up with the Jones’ and personal debt increases.

But if demand grows faster than businesses can increase output, D>S and unsustainable growth will result, with demand-push/cost-pull inflation. Thus interest rates will be raised (coupled with the extra demand for loans!). If this succeeds in gradually reducing demand the boom can be slowed into a gentle growth rate (soft landing).

Downturn

If consumers lose confidence, they stop spending money. If businesses lose confidence, they cut investment (expansions stopped and redundancies made). Shocks (such as a sudden jump in oil prices) can increase problems if they coincide with a downturn. Falling incomes, rising prices and tough credit leaves demand falling further.

Recession

If firms cut output they uses fewer resources, including labour. If earnings fall & U/E rises, disposable income will suffer, firms have less to invest and a downward spiral starts. Remember, strictly speaking a recession is TWO successive quarters of negative growth (one = a blip!).

There can be a scenario of stagflation which is undesirable – falling GDP combined with rising prices! Businesses have to contend with falling sales and rising costs, often due to an economic shock, thus some businesses might be tempted to raise their prices in desperate times! This is stagflation! (video - https://www.youtube.com/watch?v=bTz_tx460EY)

Recovery

Economies are cyclical, the dawn will follow the darkest night! Successful gov action (often gov spending), technological breakthrough, shift in consumer/business confidence….something will spark a recovery and upswing. But remember we want that upswing to be sustainable and we don’t want a rapid boom/overheating economy as this will lead to a rapid downturn!

Where would you place the UK economy in the economic cycle as of January 16?

Under John Maynard Keynes theory of ‘animal spirits’, the state of mind of producers/consumers has significant consequences for an economy. Again confidence and the psychological aspect of recessions/booms are vital to the economic cycle – ‘expectation’ can become reality.

Hyman Minsky’s theories received little attention 50 years ago until recently. He believed that financial institutions that lend money are profit seeking. After a crisis, banks/lenders are cautious only lending to those that can afford interest and repayments on capital. Over time, confidence returns and they lend to those that can only really afford ‘interest only’ deals. Eventually they lend to people that they shouldn’t have – immoral banking! Does all this sound familiar as to one of the key causes of the GFC? At some point there is a ‘Minksy moment’ when people realise that there are unrepayable debts. Panic selling sets in, housing bubbles/markets burst and this leads to crisis and recession. The cycle then starts again.

| BOOM | DOWNTURN | RECESSION | RECOVERY | |

| EMPLOYMENT | High | High, falling | Low | Low, rising |

| SKILL SHORTAGES | Frequent | Diminishing | None | Beginning |

| INFLATION | Accelerating | Slowing | Low or negative | Stable |

| CONFIDENCE | Strong | Low, falling | Very weak | Low, rising |

| INVESTMENT | High | Slowing | Very low | Growing |

Leading indicators show what changes maybe approaching – falling sales/capital equipment orders = falling confidence, falling capacity utilisation, falling consumption, lower wages and price increases are all signs of a downturn. There are some lagging indicators though (time delayed!) such as U/E which can take 12-18 months to filter through (businesses need to be sure before making redundancies or going on a recruitment drive!).

The impact of recession on firms

The impact of recession is uneven – inferior goods (negative YED, e.g. sandwich boxes) prosper, normal goods (positive YED, e.g. organic food) doesn’t. Price/income inelastic goods are necessities and are unfazed. Elastic goods are luxuries and suffer the most! When the housing bubble burst, there was a knock on effect to construction firms (construction always suffers hard in a recession), furniture stores, moving companies, etc.

Advanced planning can minimise the impact on sales/profits – e.g. supermarkets pushed their ‘own value brands’ to minimise the rise of the inferior good placed Aldi/Lidl. Producers of luxuries however have little choice but to cut costs to survive, unless they can switch resources to necessary/inferior products (e.g. Sainsburys is launching ‘Netto’ stores). In any recession, there are always opportunities and always big winners as well as big losers.

Thought Shower

A recession means a fall in the level of real national output (GDP), technically defined as two consecutive quarters of negative GDP growth. In a recession national output declines leading to a contraction in employment, incomes and profits.

The impact upon firms will depend on the industry/good/service and Income Elasticity.