Risk and Liability

Spreading risks

It is how a successful bank runs – spreading the risk associated with lending and borrowing. Remember how a bank works? The vast majority of people will have savings accounts – savings for retirement, old age, to set up a business etc. The bank depends on not everyone accessing these savings accounts at the same time – therefore the bank has money to lend out, charge interest on and make profit! It’s how a bank works – they act as a financial intermediary (a link between investors and savers). Many of these loans will be quite risky. The bank’s function is to keep very careful track of the risks involved and ensure that losses are kept to a minimum. Thus any loan/mortgage application requires a lot of information, credit-checks, bank statements, business plans etc. The bank needs to deem the requester a good investment. After lending, the bank will also watch their accounts so if it looks like a business is to make a significant loss the bank will ‘pull the plug’ and insist on speedy repayment. This may well in fact force the business to close down! But it will minimise the bank’s exposure to likely losses.

RISK = possibility that events will not turn out as expected. The probability of some risks can be calculated, by referring to past experience, but mistakes may be made and uncertainty may make calculation impossible.

A juggling act

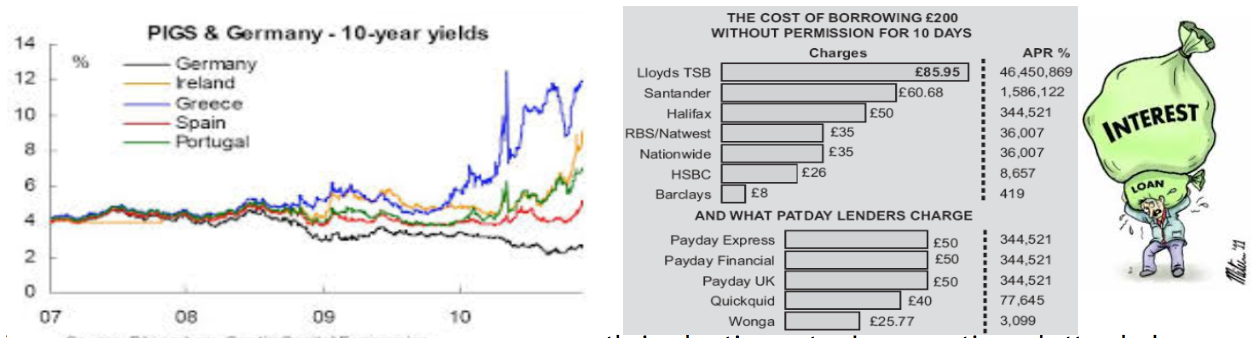

There is a trade-off between risk and safety. Risky loans are more profitable, because a higher rate of interest can be charged. So banks will take on a few risky business loans in the hope of a big profit. But there is such a thing as too many risky ventures which could lead to trouble! For example PIIGS gov bond rates vs German gov bond rates as the graph below testifies.

You may have noticed the ‘payday loans small print’ on their advertisements. In perspective, a better deal that an unarranged overdraft (this is where the high street banks can make some big money!) but still not a very good deal. No special arrangements are needed and this kind of ‘quick quid’ money is likely to be used by people who are in difficulty and would struggle to get a high street bank loan. There is a significant risk that the ‘pay day loan’ company will have difficulty getting full repayment (many take some collateral too (such as ‘The Money Shop’) or use a guarantor (such as ‘Amigo loans’)); the higher interest rate compensates them for the high risk factor.

Evaluating risks

- A bank needs to have a wide range of borrowers just so that if any one of them becomes a business failure, it is not a disaster for the bank. It is vital for any bank to spread risk. For this reason, small banks may struggle.

- Some risks can be quantified – for example a mortgage application for a doctor with a steady job and a good credit score should meet any banks algorithm for risk and it should be approved.

- Investment banks specialise in lending substantial amounts to retail businesses. This is their expertise/history.

- Banks also lend to each other, to cover deficits that are a consequence of day-to-day payments. These loans are very short term, maybe just overnight. This helps banks to keep going through short-term fluctuations in day-to-day payments. Post G.F.C, this culture of inter-bank lending dried up which deepened the G.F.C further and resulted in a ‘credit crunch’.

Impact of liability

There are a number of different legal structures for companies and these impact on the liability that economic decision makers have, thus changing the nature of risk and responsibility.

Unlimited liability

Unlimited liability means the individual has no legal separation from their business and is therefore personally responsible for the debts of the business. Their personal assets could be used to pay business debts if the business gets declared bankrupt. Sole proprietors and partnerships have this type of legal structure.

Limited liability

PLCs and LTDs have this type of legal structure – it protects shareholders as legally separate from the business. If the company goes out of business, the shareholder will only lose the value of their original capital investment (i.e. their shares purchased), their personal possessions are not at risk.

There are a few differences between Public Limited and Limited companies:

| Plc | Ltd | |

| Shares | Stock exchange | Traded privately (friends & family) |

| Share capital | £50,000 to start up | £2 to start up |

| Size | Large | Small |

| No. of shareholders | Hundreds to thousands | A few |

| Sector | Private | Private |

Why is limited liability important? New businesses are vulnerable and without LL maybe entrepreneurs would simply not take the risk. Small businesses can grow fast, provide jobs and competition – they are essential for any economy. LL (normally via a small LTD) helps to create positive opportunities.