Role of Banks in the Economy

Role of Banks in the Economy

Lending is risky business, banks need to make profits on loans to cover themselves against this risky business. But they also need to be trusted, otherwise no-one will lodge their savings in the bank in the first place and they’ll not have the capital to lend! Banks rely on the fact that not everyone will withdraw their deposits at once. But if their customers lose trust then the queues at the bank will form and the death knoll will soon sound for any troubled bank. The Northern Rock crisis of 2008 demonstrated this as well as the recent ‘Grexit’ worries of July 2015.

So the whole banking system is based on two key factors:

- Banks must act wisely so that they are able to cover the risks they take on when they lend to investors.

- Banks must be trustworthy so that depositors (savers) are confident that their money is safe.

Thus savings can be channelled towards investment in an economy with people, businesses and governments all borrowing from banks to invest and grow. This encourages economic growth and helps to raise standards of living.

Providing credit

Investment in big projects provide jobs, incomes, consumer goods, homes and other important things like roads, bridges and hospitals. Sometimes smaller projects are funded by the private sector/gov without big bank loans – but normally some kind of bank finance is required.

These investment projects have huge costs. Employees, transportation, exporting, raw materials, land, building materials, capital equipment…..there are huge ‘up-front costs’ which any business enterprise will need to meet in order to get off the ground – thus the role of banks in providing credit is essential. A good example is HS2.

The role of banks

Lending can be risky. Normally the bank will require a significant chunk of your own money as a deposit for the loan/mortgage – it acts as a deterrent for silly applications, cuts the risk a bit for the bank as they get a big sum upfront and acts a motivator of commitment for the borrower themselves.

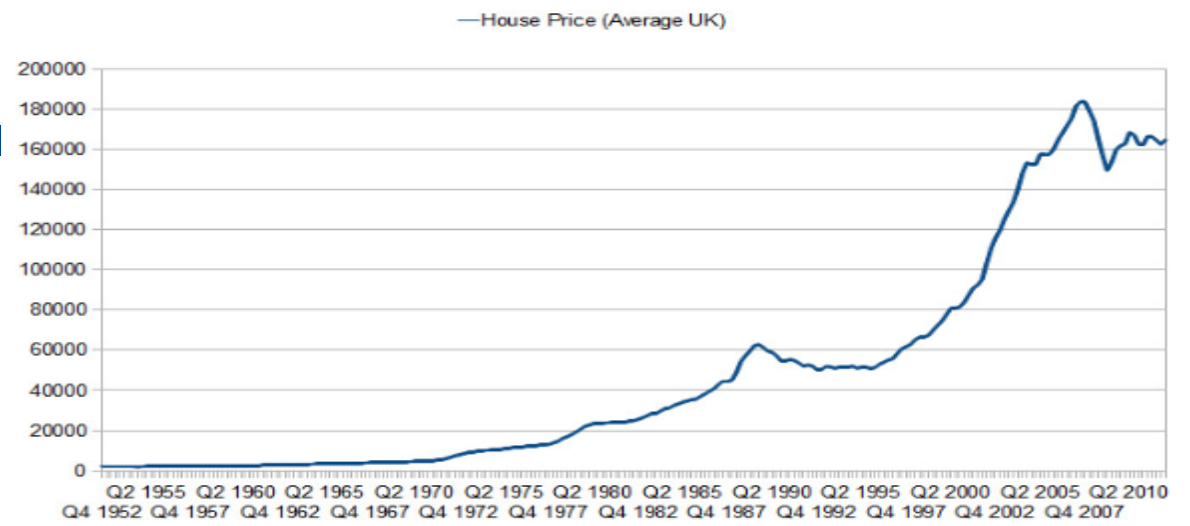

For example the norm for getting a mortgage these days is 10%-15% of the asking price as a deposit. Kent is a stable housing market and an affluent region, you’d be lucky to get a good 2 bed for £200k….that means you need a good £25,000 as a deposit!

Banks are risk adverse these days, no big deposit means no loan. Remember, if you fall behind on your mortgage re-payments the bank has the power to seize your home and sell it to repay the amount borrowed. What happens if the property bubble bursts and the bank can’t sell it for the price it was bought for? The bank will take a hit…..and some banks will struggle to survive….as did happen after the 2008 G.F.C!

Innovation in banking business

Many in Silicon Valley think that money is just another form of data, and can be managed by data companies. Apple, Fb, Google and Amazon are all looking at alternatives, but banks will fight back. Santander for example is looking at various digital services. Will a cashless society exist in the future? With the evolution from cheques and other paper-based ways to credit cards and even now contactless cards, banks clearly plan to keep a big share of the payment mechanism by competing head-on with the data companies such as PayPal, Apple Pay etc.

Overdrafts, loans and mortgages

Let’s clarify the difference here.

Bank overdrafts are short-term sources of finance (below 1 year). It gives the bank holder ‘permission to go into the red’, i.e. overdrawn and use money they don’t have. The amount and the duration needs to be agreed; going overdrawn (if un-arranged) is at a high rate of interest and usually incurs a bank fee.

Bank loads are medium-term sources of finance (1-5 years). It’s a more sizeable sum than an overdraft, for example, a car loan or other medium-term purchases. Bank loans specifically cover working capital needs (the ‘day-to-day expenses’ - there must be enough working capital to cover short-term debts). Business that don’t need to borrow as much money for such a long time may go for an overdraft rather than a fixed loan. The rate of interest is usually higher on an overdraft, though it is significantly lower sum of money.

Mortgages are a long-term source of finance (5+ years). Usually utilised for the purchase of property though businesses can ‘re-mortgage their properties’ in order to get a large sum of money so they can cure any cashflow issues. Modern day mortgages can be anything between 20 and 30 years long.

Paying for credit

Interest is charged on any amount lent – it’s how banks make profit. You have two options – a fixed rate according to the bank, or a variable rate according to the MPC (Monetary Policy Committee) of the Bank of England. Interest rates are currently 0.5%, as of Nov 2017. Though this could rise in the future, thus is the risk of a variable rate loan/mortgage.

Fixed interest rates vary according to the level of risk involved. A new business will have to pay a higher rate of interest than a well established business, simply because the bank knows that there is more risk and that a high proportion of new start-ups fail (50% fail within their first two years!). The bank charges a higher rate to try to get as much in return ASAP – so if the business does fail and declares itself bankrupt the bank won’t loose out on that much. Similarly, individuals with a reputation for paying all bills on time will find it easier to get loans at low rates.

Collateral

Collateral is the asset tied to a loan that the bank has as security against failed repayments.

Banking regulations

Since the bank fuelled financial crisis in 2008, most governments have tried to re-regulate their banking sectors to force them to ‘behave’ a bit better and less risky. So now banks are expected to be much more careful about lending and much more risk-adverse (more on this in Theme 4.5).